Why Making Money Still Feels Like It’s Never Enough

You’re making money — maybe more than you ever have before — yet somehow, it still feels like it’s never enough. This frustrating cycle is more common than people admit, and it has very little to do with how much you earn. In fact, the real issue often lies in your financial behavior patterns, emotional triggers, and invisible habits that quietly drain your resources. If you’ve ever wondered why your bank account never reflects your effort, you’re about to uncover the truth.

The reality is simple, but uncomfortable: earning more doesn’t automatically solve financial stress. Without awareness and strategy, increased income often leads to increased spending. As a result, you stay stuck in the same place — just at a higher level of consumption. In other words, your lifestyle expands faster than your wealth.

Moreover, society constantly reinforces this pattern. Social media, advertising, and peer pressure create an illusion that you should always upgrade — your phone, your car, your lifestyle. That pressure builds a subconscious belief that “more” is always necessary, even when it’s not.

The Hidden Trap of Lifestyle Inflation

Lifestyle inflation is one of the biggest reasons why making money still feels insufficient. The moment your income increases, your expenses quietly follow. You start justifying upgrades because “you deserve it,” and while that may be true, it often comes at a hidden cost: your financial freedom.

For example, someone who receives a raise may upgrade their apartment, buy a new car, or increase discretionary spending. Initially, these changes feel rewarding. However, over time, they become the new normal — and the financial pressure returns.

To combat this, many people turn to tools like the Monthly Budget Planner Pro, which helps visualize income versus expenses clearly. By seeing where your money goes, you gain control instead of reacting emotionally to spending triggers.

The Psychology Behind Never Feeling Satisfied

Another powerful factor behind this issue is psychological. Humans are wired for adaptation. This means that no matter how much you earn, your brain quickly normalizes it. What once felt like abundance soon feels average — and then insufficient.

This phenomenon is known as the “hedonic treadmill.” You keep running, earning more, spending more, but never truly feeling ahead. As a result, you chase a moving target, believing that the next increase will finally bring relief.

Additionally, emotional spending plays a major role. Many purchases are not driven by need, but by feelings — stress, boredom, anxiety, or even celebration. These micro-decisions accumulate and create a significant financial impact over time.

Emotional Spending and Its Silent Impact

Emotional spending is subtle, yet powerful. You might not even notice it happening. A quick online purchase after a stressful day, a spontaneous dinner to “reward yourself,” or a sale that feels too good to miss — these moments seem harmless individually, but collectively they shape your financial reality.

Furthermore, emotional spending creates a temporary sense of relief or happiness, reinforcing the behavior. This makes it harder to break the cycle, as your brain associates spending with positive feelings.

To address this, many individuals adopt tools like the Smart Expense Tracker App, which not only tracks spending but also helps identify emotional patterns. Awareness is the first step toward change, and once you see the pattern, you can interrupt it.

What to Do When Your Income Isn’t the Problem

If making money isn’t solving your financial stress, it’s time to shift your focus. Instead of asking “How can I earn more?”, start asking “How can I manage and multiply what I already earn?” This shift alone can completely transform your financial trajectory.

First, create a clear structure for your money. Without a system, your income will always feel chaotic. Allocate your earnings intentionally — for essentials, savings, investments, and discretionary spending. This creates clarity and reduces anxiety.

Second, build financial boundaries. Not every desire needs to become a purchase. Learning to pause before spending gives you power over impulsive decisions.

Build a System That Works for You

A simple yet effective approach is the 50/30/20 rule, where 50% of your income goes to needs, 30% to wants, and 20% to savings or investments. While not perfect for everyone, it provides a strong starting point for structure.

Moreover, automation can be a game-changer. By automatically transferring money into savings or investment accounts, you remove the temptation to spend it. This creates consistency without relying on willpower.

Many people accelerate this process with resources like the Personal Finance Mastery Course, which teaches practical strategies for managing money, investing wisely, and building long-term wealth. Education reduces uncertainty and builds confidence.

Shift From Consumption to Wealth Building

One of the most powerful transformations you can make is shifting your mindset from consumption to wealth building. Instead of focusing on what money can buy today, start thinking about what it can create tomorrow.

This means prioritizing assets over liabilities. Assets generate income or increase in value, while liabilities drain your resources. The more you invest in assets, the more your money starts working for you.

In addition, redefining success is crucial. True financial success isn’t about how much you spend — it’s about how much freedom you have. Freedom to choose, to rest, to invest, and to live without constant financial pressure.

Small Changes That Create Big Results

You don’t need a massive income to start building wealth. Small, consistent actions compound over time. Saving a percentage of your income, investing regularly, and avoiding unnecessary debt can completely change your financial future.

Track every expense for at least 30 days

Identify and eliminate one unnecessary recurring cost

Automate your savings

Set a clear financial goal

Review your progress monthly

These steps may seem simple, but their impact is profound. Consistency beats intensity when it comes to money.

Break the Cycle and Take Control

At the end of the day, the problem isn’t that you’re making money — it’s that your current system isn’t allowing you to keep it or grow it. Once you understand this, everything changes. You stop chasing income as the only solution and start building a strategy that actually works.

That said, this transformation requires awareness, discipline, and intentional action. It’s not about deprivation — it’s about alignment. Aligning your spending with your goals, your habits with your future, and your mindset with abundance.

If you’re tired of earning more but feeling stuck in the same place, now is the moment to change your approach. Take control of your money, build a system that works, and start creating the financial freedom you’ve been chasing. Your future self is depending on the decisions you make today.

FAQ – Frequently Asked Questions

1. Why do I still feel broke even though I make money?

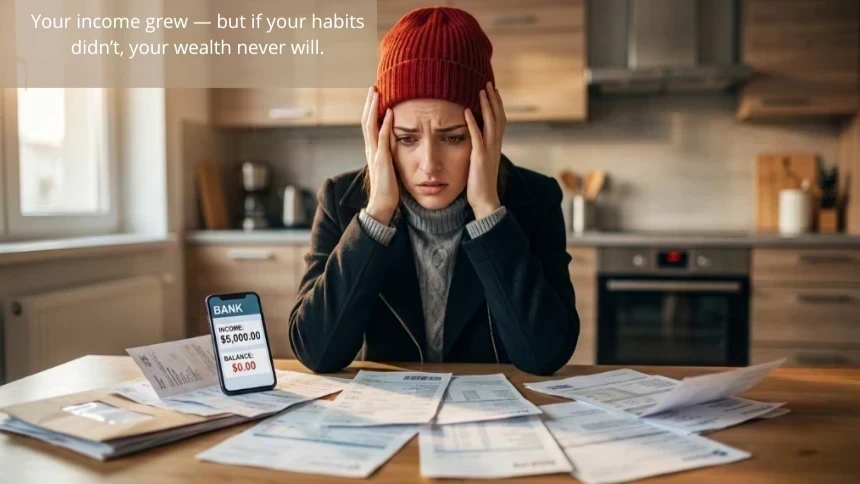

This usually happens because of lifestyle inflation, lack of clear financial structure, and emotional spending. As your income increases, your expenses often rise with it, leaving you in the same financial position.

2. What is lifestyle inflation?

Lifestyle inflation is when your spending grows as your income grows. Instead of saving or investing the extra money, you upgrade your lifestyle, which keeps you from building real wealth.

3. How can I make my money feel like enough?

You can start by creating a clear budget, tracking your expenses, limiting impulsive purchases, and prioritizing savings and investments. Structure brings clarity and control.

4. Is earning more money the solution to financial stress?

Not always. While earning more can help, it won’t solve financial stress if your spending habits and money management skills don’t change.

5. How do I stop emotional spending?

Begin by identifying your triggers, such as stress or boredom. Then create alternative habits, like pausing before purchases or setting a 24-hour rule for non-essential spending.

6. What’s the first step to gaining control over my finances?

The first step is awareness. Track where your money is going for at least 30 days. Once you see the patterns, you can start making intentional changes.

Start by observing your financial habits without judgment.

Small changes in awareness can lead to meaningful transformation over time. As you begin to understand your patterns, you’ll find it easier to make decisions that truly support the life you want.

Why Smart People Still Struggle With Money (And How to Fix It for Good)

Money Awareness Changes Everything: How One Mental Shift Can Build Real Wealth

The Emotional Side of Financial Decisions